Texas Trends 7th Edition

Inflation, Interest Rates, and What Comes Next

")

Happy (belated) New Year! Welcome back to Texas Trends. This is our first issue of 2026. Today, we’re going to explore inflation and monetary policy. We’ll also discuss some current happenings at the Federal Reserve. Let’s see how the macroeconomy is shaping up in the first quarter.

Price Pressures

January Statistics: Consumer Price Index (CPI) growth: 2.61 percent annual; 2.32 percent annualized last three months

The Bureau of Labor Statistics announced that the Consumer Price Index (CPI) rose 0.2 percent in January and 2.4 percent over the last 12 months. The core CPI, which excludes v recent disinflationary figures are promising.

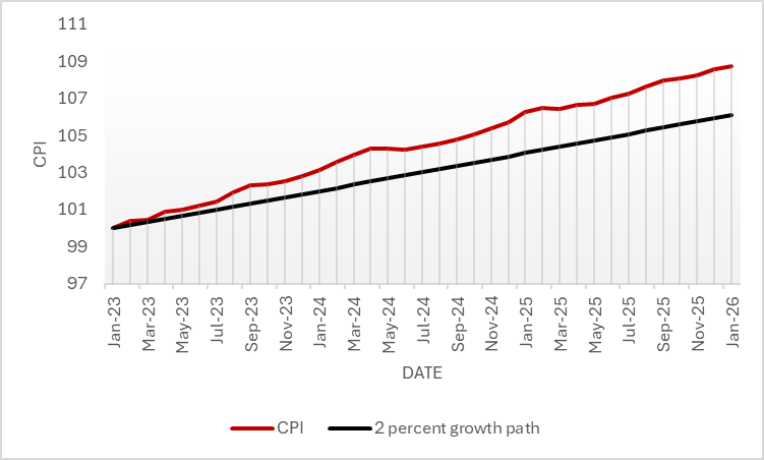

Figure 1 below shows the Consumer Price Index compared to a hypothetical 2 percent growth path. Because inflation has persistently run above the Fed’s target, prices are about 2.6 percent higher today than if monetary policy had achieved its desired inflation goal. Overall, prices have risen roughly 8.5 percent since January 2023.

Figure 1: National CPI vs. 2 percent growth path

The inflation data have major implications for monetary policy. In January, the Fed’s Board of Governors decided not to adjust the stance of monetary policy. The target range for the federal funds rate, which is our central bank’s key policy metric, remains 3.5 to 3.75 percent.

Those are nominal interest rates. They express a rate of return in current-valued dollars. What matters economically are real, or inflation-adjusted, interest rates. We can turn nominal rates into real rates by subtracting inflation. Using the headline CPI figure, the real federal funds rate target range becomes 1.1 to 1.35 percent.

To ascertain the stance of monetary policy, we need to compare the real rate range to what economists call the natural rate of interest: the price of capital that balances supply against demand. We cannot observe this rate directly. But we can estimate it. The New York Fed’s models suggest the natural rate of interest was between 1.08 and 1.56 percent in Q3:2025, the most recent figures available to us. That’s very close to the current real interest rate range. It looks like monetary policy is neither too loose nor too tight. If these data are correct, the Fed has managed to thread the needle.

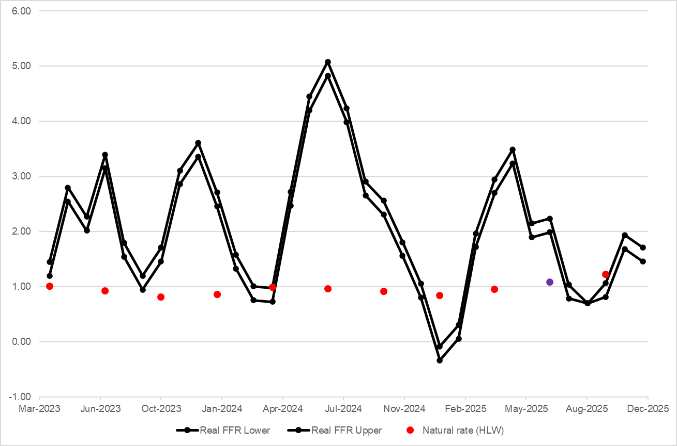

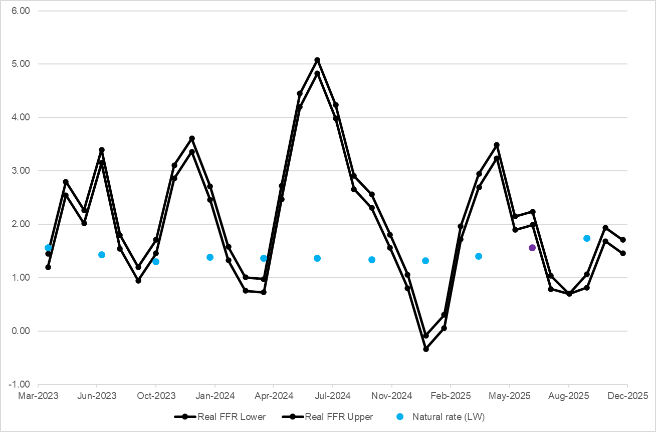

Figures 2 and 3 below illustrate this. They plot the real federal funds rate range against the estimates for the natural rate of interest. The overlap suggests monetary policy is very close to where it ought to be to promote full employment without causing inflation to accelerate.

Figure 2: Real Federal Funds Rate Range vs. HLW Natural Rate Estimate

Figure 3: Real Federal Funds Rate Range vs. LW Natural Rate Estimate

Fed’s Fortunes

Now it’s time to wade into the controversy over President Trump’s nomination of Kevin Warsh for Fed Chairman. In addition to concerns regarding institutional independence, Warsh’s nomination signals a significant change in the personal and intellectual composition of Federal Reserve leadership. Warsh received his education at Stanford University and obtained a law degree from Harvard, entering economic policymaking through financial markets and government advisory positions rather than the conventional academic economics route. (Powell, the current chair, also does not hold an economics PhD. But his chairmanship has been widely viewed by the economics profession as reflecting conventional macroeconomic views.) Before joining the Federal Reserve, Warsh worked in investment banking and served as an economic advisor in the executive branch. These experiences influenced his emphasis on financial conditions, market expectations, and institutional reliability.

Warsh does have previous experience on the Fed Board of Governors. His initial nomination in the mid-2000s was met with considerable skepticism. Critics contended that he was unusually young for the position and lacked the traditional academic background expected of central bank leaders. During his early tenure, he operated under increased scrutiny. However, his role during the 2007-8 Global Financial Crisis established him as an effective intermediary between policymakers and financial markets. This experience contributed to his distinction as a central banker attentive to how markets interpret and transmit monetary decisions in real time.

Currently, Warsh’s unconventional background sets him apart from many recent Federal Reserve chairs. While previous leaders often came from academic macroeconomics or had extensive experience within the Federal Reserve System, Warsh embodies a generation influenced by monetary instability, institutional stress, and rapidly shifting global capital markets. His public statements indicate that the Federal Reserve should adapt to structural economic changes rather than rely solely on frameworks developed during the low-inflation period of the 2010s.

Warsh has expressed an intention to reorient the Federal Reserve toward a more disciplined mandate focused on price stability. He advocates for normalizing the size of the Federal Reserve’s balance sheet, reducing dependence on extraordinary policy tools, and clarifying the realistic limits of monetary policy. According to Warsh, extended intervention risks obscuring the distinction between monetary stabilization and broader economic management, thereby undermining institutional accountability. He proposes that a more predictable policy framework, combined with clearer communication to Congress and the public, would enhance confidence in the Fed’s long-term objectives.

At the same time, the success of this agenda relies significantly on preserving independence from political influences. There are some concerns that he would be overly deferential to President Trump’s wishes for monetary policy changes, which may not be in the best interests of long-term economic stability. The Federal Reserve’s credibility depends on the perception that its decisions are based on economic conditions rather than electoral considerations. If markets perceive policy changes as politically motivated, even well-intentioned reforms could hinder inflation regulation by destabilizing expectations.ion presents both opportunity and risk.

Warsh’s generational perspective and willingness to challenge established policy assumptions may help modernize the Federal Reserve’s thinking after an unusually turbulent inflation cycle. Yet the durability of any reform will depend on whether he can preserve the central bank’s longstanding role as an independent stabilizing institution operating at arm’s length from partisan conflicts. The last thing we should want is for the Fed to become a political football.

About the Authors

Alexander William Salter is the Georgie G. Snyder Associate Professor of Economics in the Rawls College of Business at Texas Tech University and a research fellow with TTU’s Free Market Institute. He has been a member of the Red Raider community since 2015.

Jacob Walker is a graduate student at Texas Tech pursuing his Master’s in Accounting.